On March 5, the U.S. Labor Department released the jobs numbers for February, and they were phenomenal. While the expectation for jobs created was about 182,000 for the month, February saw job growth of 379,000 new hires, more than double the estimate, while unemployment dropped a tick to 6.2%, and the numbers for January were revised higher by an additional 117,000 hires. The day before, Fed Chairman Jerome Powell signaled that although they see signs of “transitory inflation” in the economy, they’re not prepared to ride to the rescue just yet with any new interest rate hikes. In addition, the Atlanta Federal Reserve is currently predicting first quarter growth of a whopping 8.3% as of Friday, a pace of growth that rivals that of even serial exaggerator China. For some context on this, typical GDP in a bull market is around 3.2%. As such, surging growth of 8.3% is insanely good, even as it raises the long-term possibility of an overheated economy.

So with all of this good news marinating throughout the economy, why have markets been so jittery in recent weeks? The answer lies in spiking Treasury yields and the specter of inflation. Interest rates have risen steadily to the point where the yield on U.S. 10-year Treasuries is now a whopping 1.61%, up from 0.498% a year ago. (With most countries in the G-20 averaging less than half of that, others are still in the negative.) Markets are viewing these interest rate spikes as threatening to equities, in part because there are signs of inflation throughout the economy. Food and gas prices are up substantially since the new administration was inaugurated, impacted by the suspension of construction of the Keystone XL pipeline, the cessation of oil and gas leases on federal lands, and other equally destructive job-killing policy implementations. Anyone looking to buy a house in the last year has faced the competition of multiple cash offers, often tens of thousands of dollars above asking price, and inventory is extremely limited.

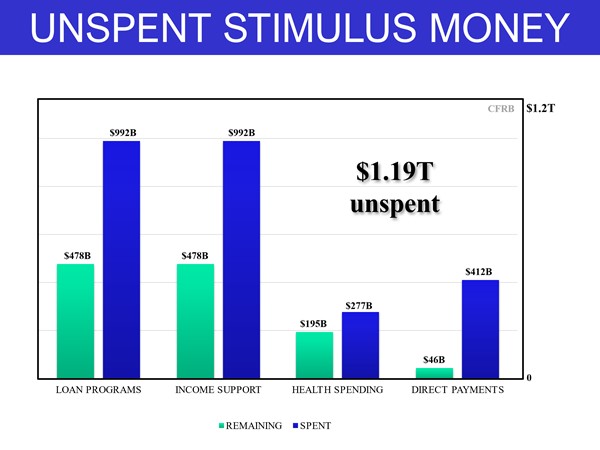

Then last Friday, investors awakened to the news that Vice President Kamala Harris had just cast the tie-breaking vote in a 50-50 divided Senate for President Biden‘s $1.9 trillion “Covid relief” bill, a boondoggle of pork and unrelated handouts to blue state governors and mayors, with only 9% of the bill actually earmarked for Covid relief this year. This despite the $1.2 trillion from the first 5 relief bills that hasn’t even hit the economy yet.

Markets view such extreme over-spending as irresponsible and inflationary, and the concern has been consistent over nearly four weeks now: Too much “free” cash in the hands of spendthrift consumers could create a super-heated economy, reignite inflation, and see a market crash in the hangover that inevitably follows—all while adding dramatically to our national debt. While we do not yet see capitulation, the market has definitely retreated from its bullish optimism of the last five months.

For much of the last five years, the acronym TINA (There Is No Alternative to stocks) has been the rule on Wall Street. With the Fed keeping interest rates at record lows, bonds have certainly been no threat to stocks which have risen dramatically amid the business-friendly policies of the last administration. Institutional money managers, especially those managing pension funds, have been overweighted in equities for years. Employer 401(k) plans have grown nicely, adding to personal wealth and boosting the pre-Covid economy to the strongest in American history through February of 2020.

Now, after many months of lockdowns, American small businesses—the engine of job growth in our economy—are finally picking themselves off the floor and reopening nationwide. As of this writing, U.S. Covid cases are down over 77% in six weeks, and 15 state governors have now rescinded their state’s mask mandates (see map), even as they and others have reopened large parts of their economies.

Legislation is pending in others outlawing lockdowns by counties or cities. Florida has been open for months and their schools have been open since last September—sports programs included—based on the science put forth by the CDC[1] and other worldwide health organizations proving that Covid is not communicable from children to teachers. As the nearby chart shows, total U.S. deaths (from all causes, Covid included) as a percentage of the population were only marginally worse in 2020 than the year before, entirely in line with a 10-year trend of minor increases. As more and more Americans are educated to these facts, and as the vaccines are distributed to those who want them, our economy should once again thrive—but will the stock market follow? Historically, bull markets last an average of 3.8 years and it has now been 12 years since we had a (non-Covid related) bear market decline of -20% or more. On that basis alone, many investors are inclined to lock in their gains and wait out the Biden administration’s announced tax hikes, relaxed immigration policies, increased regulation on business, and the inflationary $1.9 trillion spending bill that just passed the U.S. House and Senate without a single Republican vote.

If you’re over 58 years of age, approaching or recently entering retirement and find yourself overly exposed to these dysfunctional markets with money that it’s taken you four decades to save, now may finally be the time to take some risk off the table. When markets are this undecided, there’s never a bad time to take a profit, and the rally of the last two sessions may be the ideal time.

If, in addition, you also have genetic familial longevity and are concerned about outliving your investments in your latter years, we specialize in solutions that prevent that from ever happening. Our typical new client, after multiple diagnostic, educational, and implementation meetings, elects to protect a minimum of two-thirds of their assets from risk, often allocating them to guaranteed lifetime income solutions. As such, even if the other 30-35% of their investments were to lose half of their value in the next crash, their overall balance would only be down -17%, an easily recoverable loss over a 20-year retirement.

For more information, contact our office at 603-595-4990. As always, we welcome your comments.

[1]Note that when the CDC first announced last August that only 6% of “Covid-related” deaths in the U.S. were Covid-ONLY, and the other 94% of Covid-related deaths showed an average of 2.6 other comorbidities, their updated data is now showing an average of 3.8 other causes of death, in addition to the presence of antibodies (from an earlier infection) or the virus itself when an autopsy is performed. Ex.: A 79 year-old male died of a heart attack, with COPD, as an overweight diabetic, and the autopsy revealed the presence of Covid antibodies from an infection months earlier. Such deaths are considered “Covid-related” and make up 94% of all reported Covid deaths.