By Thom Brueckner

If you’re like most investors of the last 12 months, you’ve been scratching your head, wondering at the direction of markets amid the Federal Reserve’s relentless push toward higher interest rates in an attempt to curb the inflation they once thought was “transitory”. The market has essentially been trading within the same 2000-point range for the better part of 14 months, and the first 1500 points of last week’s selloff had everything to do with rising treasury yields and nothing whatsoever to do with the failure of Silicon Valley Bank. (Another subject for another blog.)

After the Great Financial Crisis in March 2009, the Federal Reserve dropped interest rates to 0-0.25% in an attempt to restore liquidity to the world economy, make the cost of borrowing as inexpensive as it had ever been, and give banks time to recoup their real estate losses. As Mae West once said, “too much of a good thing is wonderful” and as the Fed kept rates low for far longer than we now know was prudent, they basked in the gratitude that investors showered up on them. With nothing to compete with annual historical equity yields of 8.3%, dollars left 0.3% yielding CDs and 0.9% yielding bond funds for stocks and equity mutual funds, citing the acronym TINA (There Is No Alternative) as justification. Stocks naturally soared, averaging well above historical averages for over a decade.

Fast-forward 11 years to the coronavirus pandemic, and the Congress’s and Federal Reserve’s entirely inappropriate response to it. As Rahm Emmanuel once famously said to President Obama years earlier, “we should never allow a good crisis to go to waste,” the words of a chief of staff encouraging his boss to hide a political agenda within the solution to a systemic crisis. Nancy Pelosi and her Democratic colleagues used the power of appropriation given to the House of Representatives by the Constitution to appropriate bailouts totaling over $6 trillion for various needy parties, constituencies, teachers unions, airlines, and anyone else needing relief from the self-imposed shutdown of our economy in the face of a raging pandemic. As if all of those targeted bailouts were not enough—and in spite of the fact that “the crisis was over“—the outgoing Congress last year passed an enormous $1.7 trillion Omnibus Spending bill, claiming its necessity to solve the “environmental emergency” that they had earlier claimed would end the planet within 12 years.

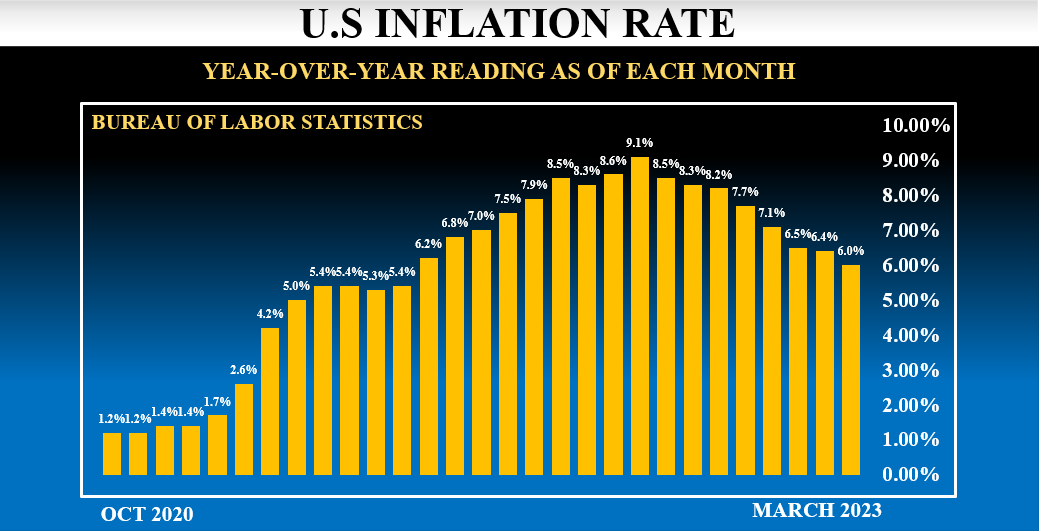

Where to from here? On the one hand, we have the Federal Reserve, like firefighters with massive fire hoses putting out the flames of the hyper-inflationary $6 trillion congressional overreaction to the pandemic while, on the other hand, the Biden administration and the last Congress have filled the tanks of an additional $1.7 trillion flamethrower with a monetary propellant that they have yet to spray over the domestic economy. Is there any wonder then that the inflation the Fed is attempting to mitigate has barely budged, dropping to 6.4% from 6.5% last month, and rising 0.4% month-over-month on Tuesday of this week? Prior to the distraction of the Silicon Valley Bank failure/rescue, markets had reacted negatively to Jerome Powell’s most recent testimony before Congress, a speech in which he reiterated what the Federal Reserve has been saying all along—but that markets have been reluctant to believe—namely that the Fed is steadfastly devoted to its mission to continue raising rates for as long as it takes to tamp down inflation.

At the end of the day, of course, the Fed’s actions will eventually stall the economy enough to create what they hope is only a mild recession, a “soft landing”, one just punishing enough to bring prices back down to normal and, after a long pause to allow the economy to absorb all of the pain in the pipeline, they’ll eventually begin lowering rates again. What the market has missed in all of this is that the Fed has no intention of bringing rates back down to the levels of 2009 through 2020, that wonderful 11-year period where markets seemed to only go up, and where the Fed continued to spike the punch bowl and keep the party going with record low rates. Instead, a return to historically normal interest rates is the more likely course of action, meaning that now and for the foreseeable future stocks will no longer have a monopoly in the yield department.

Why, if a six-month treasury bill is currently paying the certainty of 5.1%, would a prudent investor choose the possibility of 8.3% instead, when that historical S&P 500 average annual return is accompanied by the average bear market decline of -41%? Put another way, when certainty begins to approach the attractiveness of possibilities with risk, why wouldn’t a prudent investor take some risk off the table and reallocate a portion of their account to that certainty? No matter when the recession begins, how long it lasts, what the eventual terminal interest rate of the Federal Reserve may be, how long they leave it there, and when they will finally begin cutting again—none of these things matter. The only thing that matters is that stocks, once again, have competition for yield. As my producer says in the open to our radio show, “you no longer have to risk your money in order to grow it…”

For the last 11 years, whenever retirees and pre-retirees are polled about their greatest fears around retirement, the #1 answer has been “Running out of money.” Their #2 answer now is “Another major market crash” just prior to or just into retirement. Speaking as the owner of a firm that specializes in Retirement Income Planning, I have never seen the solutions we design illustrate so favorably in my entire 32-year career. As is the case with treasuries and other interest-sensitive instruments, Guaranteed Lifetime Income (GLI) vehicles are now highly favorable, with the top products showing yields above 7% after just two or three years of deferral, guaranteed for life, even if that client or their spouse lives long enough to run out of money. You read that correctly. In this interest rate environment, consumers now have a choice between the casino on Wall Street, where market history is 8.3 %/year fully at risk—or the certainty of over 7% with no market risk whatsoever.

As Bill Belichick once asked his now-famous quarterback, “If you’ve already won the game, why are you still out on the field?”

7 Comments

Thanks again, Thom, for your truthful insight into our chaotic world nowadays.

Peter,

I appreciate the compliments. Thanks for commenting!

Thom

If you have money in a bank account would you leave it in that account or withdraw the money?

Hello Roy,

The FDIC insures deposits up to $250,000 at any bank, whether a small regional bank, or one of the Big Five. What you’re reading about in Silicon Valley are the larger depositors who had well an excess of that insured amount at stake at Silicon Valley Bank, and several others that have since been seized by regulators. If you have less than that, the government is assuring you that your deposits are fine, and that the banking system is stable. If you have more than that in any one account, you may want to spread it out among several banks in increments of less than $250,000.

Hope you’re well,

Thom

Great post, Thom.

Glad where our money is sitting without loss or worry as the Biden wrecking ball continues to plunder the country.

All the best.

Nice job, Thom 👏

Love the Belichick analogy 🙂