Fact: We are now several months into the 13th year of an ongoing* bull market, which began—courtesy of the Federal Reserve’s ZIRP (zero/low interest rate policy) on March 9th of 2009. Apart from this merely being a curious factoid, why is this significant?

Well, for starters, it behooves us to note that the average bull market lasts 3.8 years, and when the market does go into bear territory (a loss of more than -20% from the recent high) its average drop is -41%. This begs the question: How many 58-65 year-old investors, with retirement looming up ahead, can afford an average loss of -41% of the monies that it’s taken them four decades to save? Not many.

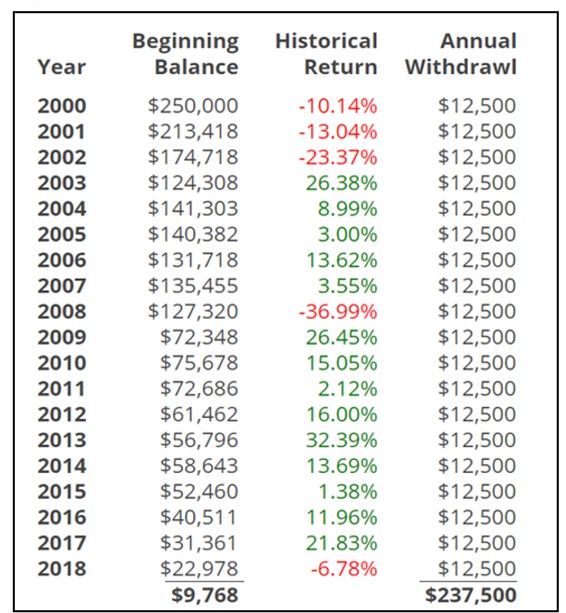

As the chart below shows, a 65 year-old couple who retired in 2000, and withdrew only 5% of their then balance per year over the next two decades—while leaving their money fully invested in the S&P 500 Index—saw their values halved in only four years. Although the 2000-20 era was one of the more robust periods in U.S. stock market history (only 5 down years offsetting 14 gain years), these retirees were completely out of money at 84, after only 19 years in retirement.

One question that I often ask in our Retirement 101 classes when speaking to attendees pending retirement is this: “How many of you would be willing to give up some of your gains every year, in exchange for never losing money in the market again?” Virtually every hand in the class goes up. I then follow that up with a second question: “Okay, how many of you would be willing to give up half of your yearly gains, in exchange for never losing money in the market again?” Almost every raised hand in the room goes back down.

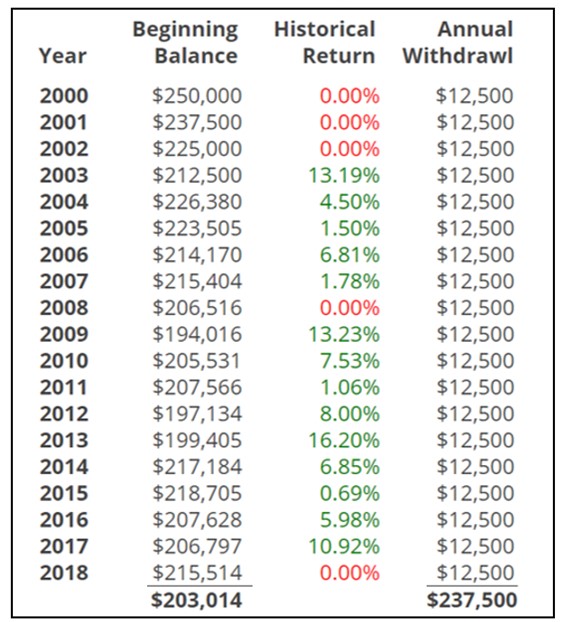

As the revised chart below shows, eliminating losses, even when at the expense of having one’s gain years cut fully in half, has a dramatic effect on the sustainability and longevity of one’s retirement income. After taking out the same $237,000 over 19 years, the couple who eliminated their losses still has over $203,000 left in their 19th year of retirement at the age of 84. In 19 years, they’ve only reduced their account balance by $47,000—even though they withdrew $237,500 during that period. Put another way, they were able to spend over 95% of their year-2000 account balance, but 20 years later they still have over 81% left for their sunset years, their heirs, or for charitable intent.

With a new administration promising record tax increases, commodity prices up as much as 300% in one year, worrisome inflationary indicators pinging throughout a struggling economy still straining from the recent pandemic lockdowns, we’re coasting into the 13th year of this bull market and few if any are asking, “What could possibly go wrong?”

Even if you believe that our economy is structurally sound, consider the geopolitical risks currently posed by an emboldened China, a meddlesome Russia, the renewed threats of war in the Middle East, and countless other recently flaring hotspots of concern around the world. Any one of these could become the next “Black Swan” event—like the once-in-a-hundred-year pandemic that no one predicted in the fall of 2019—that triggers a decade like the 2000 through 2009 era shown in the charts above.

When asked recently what a pre-retiree should be doing in this climate, one commentator on a popular business channel replied succinctly: “Sell half. Do it in your IRAs where there’s no tax consequence, and leave the other half to ride out the market. By so doing you lock in your gains of the last 13 years, avoid future losses on the entirety of your portfolio, and give the remaining half room to grow further should the markets keep rising.”

There’s one final point to be made: Life expectancies are increasing each year and over 70% of the people we meet with annually have as their primary concern the fear of outliving their money. Only 36 percent are very confident they will be able to retire comfortably. Many are delighted to learn that there are custodians who will guarantee them a lifetime income, one that continues even if one or both spouses live long enough to actually deplete their accounts.

For more information on how to avoid market losses, insure against the unexpected, and guarantee yourselves an income for life, give our office a call at (603) 595-4990.

Warmly,

*NOTE: The government-imposed lockdown of the economy in February of 2020 resulted in a market loss of -37% in 5½ weeks but did not have structural roots in an economic cycle or a causal decline, and is therefore dismissed by most market-watchers as not a true or conventional bear market. Reversing course and rising over 20% off the March 23rd bottom in only three trading days—defined as the start of a new bull market—further dismisses the decline as an illegitimate bear.